Financial wellbeing is the state of someone’s financial health and overall satisfaction with their financial situation. Financial wellbeing goes beyond just making money, it concerns money management, handling financial challenges and making informed decisions on income, expenses, savings, and investments for future financial security.

With increased financial uncertainty and an ongoing cost of living crisis, the relevance of financial wellbeing has reached new heights. Employees are faced with challenges such as continued rising food and living expenses and stagnant wages; understanding the importance of employers promoting and supporting financial wellbeing has become crucial to meet evolving needs.

Financial literacy

People who have high levels of financial literacy have the knowledge and skills necessary to make informed financial decisions and build solid foundations for the future.

The UK has a financial literacy level of 67%, whilst Ireland only reaches 54%, according to a recent survey by Bank of Ireland. These figures indicate support may be required to improve financial literacy levels and protect and maintain financial wellbeing.

Money Management

(IRL) 60% of Irish people are currently in debt, with 1 in 10 describing their debt as serious. 49% of Irish adults don’t feel confident managing their money, with almost a fifth (18%) being sometimes or regularly overdrawn in their personal accounts. The cost-of-living crisis impacts are felt community-wide as 18% of Irish households that are considered to be at the higher end of the income spectrum describe themselves as struggling or stretched with finances.

MoneySherpa research has revealed that consumers in Ireland have up to 20% less financial literacy levels than some other European countries. This is backed by findings from a 2023 CCPC report that states only 50% of Irish consumers keep money for bills separate from day to day spending money and 35% of people don’t make a plan to manage income and expenses.

The state of the economy and the current cost of living exceeds the wage’s capacity to cover the essentials. It is becoming clear that despite money management skills and strategies, achieving positive financial wellbeing is proving difficult.

According to research by An Post 87% of people in Ireland have concerns over their current financial wellbeing and 65% report increased anxiety over essentials and household bills. 1 in 5 people report the price of groceries being their main financial concern, an increase of 38% since January 2023. Anxiety over groceries is due to a 13.1% increase in the price of food in the year to April 2023, according to the CSO Ireland.

Almost a third of parents in Ireland have skipped meals or dramatically reduced portion sizes in the past year to feed their children. Further research from Barnardos shows the number of parents using food banks and relying on food donations has doubled. The rate of food price inflation is the highest it has been in 15 years, costing the average Irish household €1159 more for a year’s worth of groceries in 2023 (totalling €8270).

Finances & Mental Health

Finances and mental health are intricately connected with one significantly impacting the other.

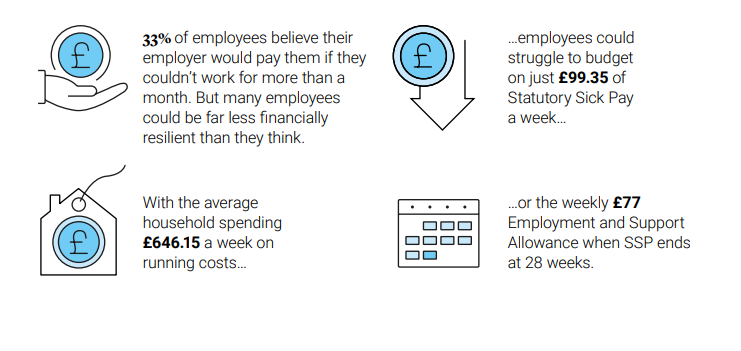

33% of employees live pay day to pay day, and 1 in 5 households are just one payday away from financial disaster.

Financial difficulties such as debt, unemployment/reduced hours or salary not stretching far enough can create a burden on people causing anxiety, depression and helplessness. These symptoms experienced over time can lead to a long-term and serious mental illness. Similarly, some people with mental illnesses may make poorer financial decisions i.e purchase on impulse or through periods of hypermania in an attempt to feel better. Depression or excess stress can affect decision-making abilities and motivation making it difficult to manage finances properly.

According to Money and Mental Health, half of the people in problem debt also have a mental health problem. Almost 40% of those with a mental health problem say their financial situation worsens it. This is backed up by research conducted by PayOff found that nearly 1 in 4 suffer from PTSD like symptoms caused by financial distress, showing how extensive mental health implications can be.

A recent survey from the Mental Health Foundation touches upon how other areas of mental health/wellbeing can be affected, illustrating how crucial a holistic approach to wellbeing is. The survey revealed that:

- Almost 1 in 3 adults is experiencing poorer quality of sleep as a result of financial worries.

- Almost a quarter are meeting friends less often.

- People are engaging less with their hobbies and overall reducing their amount of exercise.

2023 Laya’s Workplace Wellbeing Index Report revealed that in Ireland, finances and the cost of living are causing 20% of women and 12% of men to feel anxious all the time.

How does this all tie into each other?

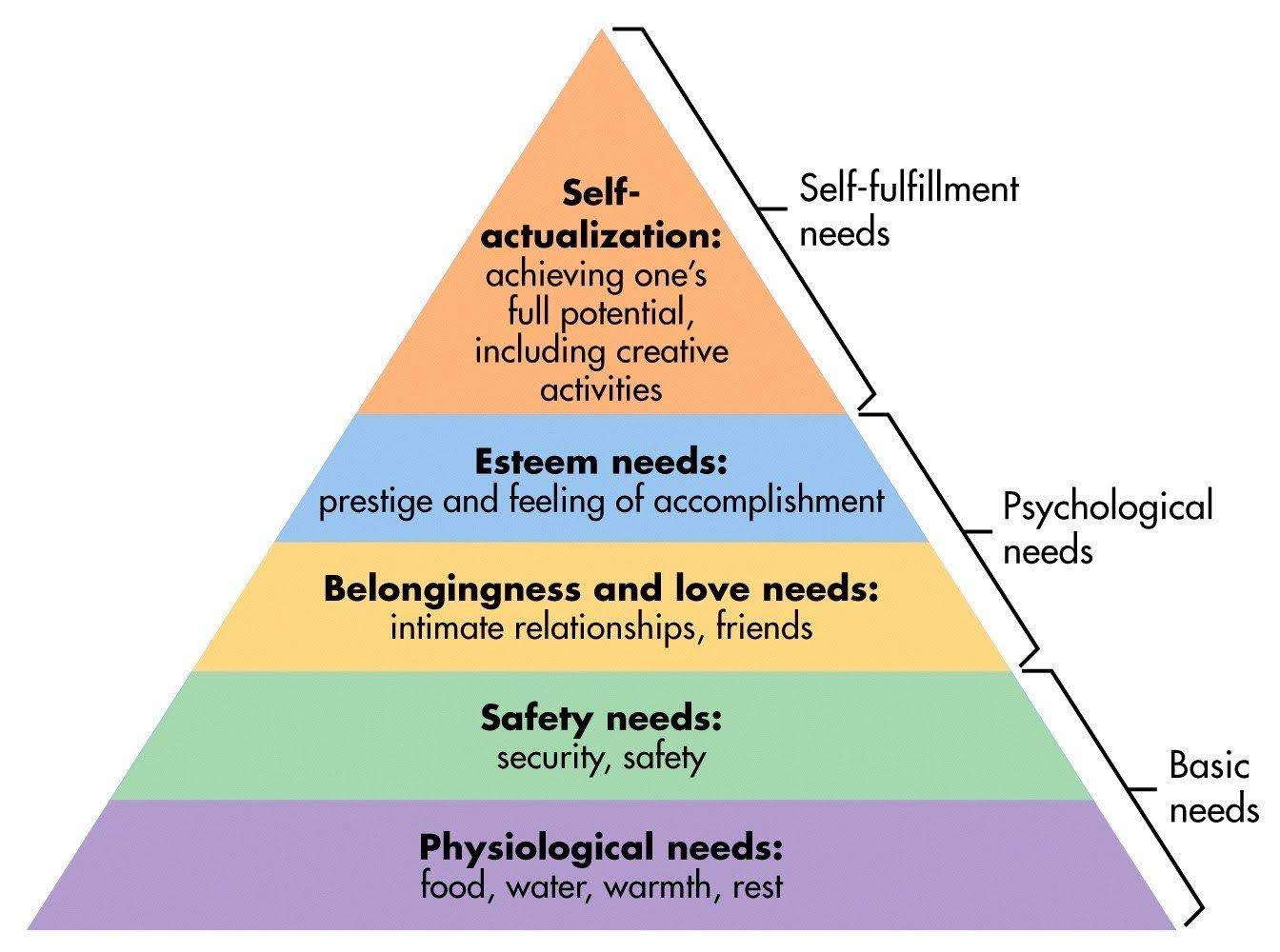

Abraham Maslow is an internationally famous psychologist that came up with a theory called the Hierarchy of Needs explaining human behaviour and motivations.

Despite this theory being first introduced in 1943, it is still relevant today and useful when used as guide for awareness and motivation.

The hierarchy of needs teaches us that basic needs must first be met so people can realise and achieve their full potential. Maslow argued that failure to meet needs at various stages of this model can lead to both physical and mental illness.

This diagram shows that if an individual’s basic needs aren’t met such as good quality rest/sleep, getting enough food they aren’t in a position to start catering for their mental health and wellbeing needs as the person is more focused on survival. The previous Mental Health Foundation research highlights this as people are less focused on socialising, doing things they like and exercising for overall health.

As the economic situation shows no signs of stabilising, financial anxiety increases across the board. It is becoming increasingly more difficult to maintain a positive state of mind/wellbeing as basic things such as getting enough food for yourself and your family can be unachievable in the current economy. Many are struggling to cope and keep afloat in the short term, with rising stress over how this affects future financial stability.

From an employer’s perspective, the Hierarchy of Needs explains that employees are unable to come to work motivated if basic needs aren’t met or stress/anxiety exists over financial wellbeing and covering the essentials. Employers should recognize the impact of financial stress on productivity and take proactive steps to provide comprehensive financial wellbeing programs.

Finances & Financial Help

Struggling to cope financially leaves many in fear and not knowing what to do. Individuals and families seek expert advice and guidance to help navigate the various financial challenges they are experiencing.

Strained budgets mean people need to make better informed financial decisions, when and where possible. Demand for financial advice has increased as people strive to optimise their level of income and attempt to plan for the future where possible.

Incoming calls to Spectrum.Life’s mental health services for financial concerns and incoming calls to Spectrum.Life’s specialist financial advice soared by 77% between January and October 2023 compared to same time last year.

Financial 101 was the number 1 most booked Wellbeing Series class in 2023.

Data (May 2023) from StepChange (a debt advice charity) shows:

11% increase (May 22-May 23) in the number of new clients accessing debt advice identified the cost of living as the most common reason for their debt.

1 in 3 clients have a negative budget which is unchanged month on month.

3 in 5 clients are in some form of employment, illustrating salaries aren’t stretching far enough.

For younger cohorts or those struggling and not knowing where to turn for fear of additional costs, there has been a rise in the use of social media to get financial help and advice. People are turning to ‘Finfluencers’ for advice. Finfluencers are social media influencers with large followings/engagement that give investment information/advice and advice on a range of topics such as stock market trading, saving, personal finance and mutual funds.

Finfluencers are becoming more prominent on social media with many gaining credibility based off their cultural status or popularity.It is important to reach out for specialist and professional advice to ensure you make the best financial decision for yourself and family.

Some finfluencers may not be true experts in their field and can be sponsored/paid to sway decisions and promote specific services. Online investment scams have soared recently with young people being most at risk, according to recent Barclay’s bank data.

Barclay’s also reveal that 77% of all scams take place on tech platforms like social media with the average amount lost to investment scams by young people being £3692 – the equivalent to a year’s student loan.

This has caused many financial institutions, services and authorities to make a plea to the public to check all investment decisions over and do due diligence before investing.

Employer Support

The current economy presents a range of risks that impact the financial wellbeing of the workforce. 73% of employers believe that the cost-of-living crisis is having an impact on overall workforce wellbeing. Managing employee wellbeing is being pushed to the front of agendas to tackle financial distress and try to reduce the amount of in work poverty.

In fact, 1 in 8 employees are already experiencing in work poverty meaning that after an employee has paid housing bills and expenses, they don’t have enough disposable income to meet the current cost of living.

Management and managers have a crucial role to play in supporting employee wellbeing and should be equipped with the right tools and skills necessary to do so. New research from Mintago reveals that UK businesses are currently failing to provide sufficient financial wellbeing support.

Mintago research also found that almost 9 in 10 (87%) of senior managers have been approached by an employee in the last 12 months to discuss wellbeing concerns. Out of those managers that discussed finances with employees, 68% of employees stated the cost-of-living crisis was the biggest cause for concern with 50% requesting a pay rise and 43% of people worried about debt.

Managers are often the first point of call for employees reaching out for support, yet 47% felt uncomfortable on a personal level handling financial concerns. Training in this area may be required to ensure employees on all levels feel supported and wellbeing is protected as much as possible. Managers own wellbeing may suffer if they do not feel equipped in dealing with these types of concerns, particularly if they’re struggling financially themselves.

Presenteeism in many industries has increased with 64% of employees with in person roles having to attend work because they can’t afford any income loss with around 4 in 5 admitting to working through illness. For healthcare and social assistance staff, around two thirds have had to do the same. When employees attend work when unwell, other staff are put at risk and overall mistakes increase while productivity/efficiency suffers, costing employers more in the long run.

Increased presenteeism may result in increased staff burnout which poses higher risks for both employee and employer should conditions deteriorate further. For those that are able to take time off work. 4.2m worker days are lost each year to a lack of financial wellbeing- equivalent to £626m on average in lost output.

Due to the cost-of-living crisis, 11% of UK employers are allowing employees to use employer pension contributions for other financial priorities- 22% are planning to introduce this level of flexibility within the next 24 months. Flexible solutions help support a diverse workforce and enable higher levels of productivity and reduce presenteeism all round.

Employers are recognising the relationship between wellbeing and productivity with nearly 7 in 10 employers believing staff performance is negatively affected when employees feel under financial pressure. 34% of employers are set to increase financial wellbeing spend during 2023, despite this, just 14% of employers have a mature strategy that is integrated into company culture for financial wellbeing.

It is shocking that 48% of employers currently do not offer financial wellbeing benefits/services, and the 52% that do, do not have them joined up in a strategy. Financial wellbeing support is an imminent concern for employers as 60% of employees expect their employer to provide some type of financial wellbeing benefit and 35% would move elsewhere for better pay and benefits.

CIPD found that 40% of employees in an organisation with financial wellbeing policy do not feel their employer is doing enough to support financial wellbeing. Organisations that do offer financial wellbeing benefits as part of their wellbeing policy need to proactively and regularly evaluate how employee’s needs are being met.

Group Income Protection

The cost-of-living crisis is having a huge impact upon the lives of many people in the UK. Costs are rising faster than our wages, things like energy bills and weekly shopping take up a larger proportion of household budget. This means more of employees are experiencing financial difficulties, and we know that money worries can have a big impact on our physical and mental wellbeing.

From an employer perspective we believe Group Income Protection (GIP) is a crucial part of an employer’s wellbeing strategy and providing that extra security, during these challenging times. Our wage is an individual’s largest, and most important form of income. GIP is designed to help ensure employees and their families are supported financially, practically and emotionally when they’re unable to work long-term due to illness or injury.

Some stats: (Legal & General GIP)

On top of the financial pay out an employee receives through GIP (where applicable, It also offers extra wellbeing services which employees and their families can access to take care of their day-to-day wellbeing, including their financial wellbeing.

Keeping Employees Healthy

Most GIP insurers will provide immediate support to employees via online GPs, Employee Assistance Programmes (like Spectrum.Life), and other specialist health providers. These early interventions provide quick support when it’s needed and can help prevent issues getting worse before they lead to long-term sickness.

Helping Employees get better

Those that do go absent from work are, if appropriate, actively managed and provided with vocational rehabilitation to help them get better and return to work. This includes working with employers to adapt workplaces to help manage a successful return to work.

Support for those who are long-term sick

And as mentioned, GIP insurers will pay a regular income to help financially support employees who can’t return to work because of long-term sickness or injury.

What can we do?

The first and most important step is to understand your employee needs, conduct research to gather insights on your workforce including their needs/challenges and identify areas where support is required. Before creating any financial wellbeing strategy, employers must ensure it is valuable to the employee and not going to be a waste of effort or resources for any potential investments.

Increasing pay seems obvious, but is it doable given the impact is felt all round?

Ensuring financial wellbeing benefits and support will help meet employee baseline needs and increase overall productivity and enhance employee engagement, supporting the overall wellbeing of their workforce.

Organisations that prioritise holistic wellbeing support including financial wellbeing benefit from reduced turnover and improved retention. Proactively addressing financial needs helps to create a supportive environment that encourages employee wellbeing and loyalty, helping to protect overall mental health and allow cost saving associated with recruitment, training and onboarding new talent.

Providing financial wellbeing solutions like access to discount platforms that potentially help save costs on consumer goods. Help employees take care of themselves with healthcare plans, may be provided to ensure mental and physical health remains optimal as health priorities may slip in times of distress.

Robust EAP offerings will enable employees to make use out of counselling/therapy services, with many including extensive debt management advice without the need for another third party offering or additional cost. Financial advice or counselling for budgeting or debt worries are essential on a base offering to reduce levels of anxiety of stress and help employees maintain productivity and performance levels when in work,

EAP offerings include access to many wellbeing solutions like meditation, nutrition and sleep advice to help common symptoms suffered by those experiencing money difficulties and make money stretch further.

Salary sacrifice benefit schemes where employees pay for a product/service before their wage comes in, allows them to save on tax contributions. Similarly, participating in earned wage access schemes (EWA) can enable real time access to wages to give struggling employees more freedom with their finances.

Training and workshops could help management open conversations and reduce stigmas within the workplace, making it easier for employees to seek help and not feel so isolated.

Greater flexibility will help ease the pressure put onto unpaid carers and help protect women in employment whilst trying to balance work and child responsibilities. In contrast, there may be employees that wish to work in the office to save money on household bills if they were to work from home.

Remember, change starts with culture. If people are comfortable enough to speak up and voice their concerns or challenges, others may be encouraged to do the same. Sometimes hearing someone going through a similar situation is enough to help people along the way. Employers will get better insights into employee needs with a more supportive working environment, when people feel their best, they perform at their best.

If you would like to discuss a financial wellbeing strategy for your people, contact wellbeing@spectrum.life today.